key insights

- Regulators are no longer monitoring stablecoins in isolation, but also in the context of overall financial regulations.

- The main interest is still USDT due to its popularity in cross-border transfers and internal trading.

- The level of enforcement going forward is likely to be determined by the definition of “high-volume transactions” and “suspicious activity” that will be used.

Thailand’s stablecoin monitoring has begun a challenging time as the Bank of Thailand and Securities and Exchange Commission have collaborated to scrutinize USDT transfers on a larger scale and enhance anti-money laundering enforcement measures. The campaign expands its scope to cash transactions, foreign exchange conversions and gold transactions, as regulators try to cut down the illegal financial networks and the mushrooming gray economy in the country.

The move is part of Thailand’s progressive stance on cryptocurrency. Although cryptocurrency trading is legal, government authorities are stepping up their regulatory efforts over illegal financial transactions connected to digital assets. This has the potential to impose more compliance requirements for exchanges, financial institutions and those large transaction participants.

Authorities widen oversight across digital assets and cash networks

According to local reports, Bank of Thailand Governor Vitai Ratanakorn said the campaign will rely on several long-term enforcement measures instead of temporary actions. Regulators have already started reviewing high-volume stablecoin transfers, with USDT receiving particular attention because of its widespread use in cross-border payments.

Officials believe stablecoins allow funds to move quickly across jurisdictions, making them attractive for individuals attempting to avoid traditional banking controls. Consequently, authorities are applying data analytics to identify unusual transaction patterns and transfers that may indicate money laundering or other illicit activities.

At the same time, regulators expanded monitoring across several financial sectors.

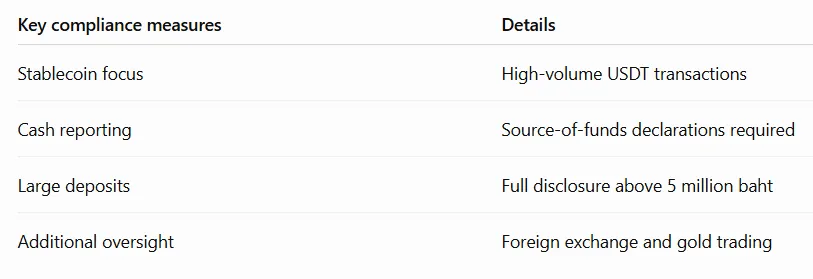

The strengthened compliance framework includes

- Source-of-funds declarations for high-value cash transactions.

- Better monitoring of any large exchange of bank notes without a business purpose.

- The cash deposit is required to be reported fully if it is more than 5 million baht (about $150,000).

- Increased oversight of transactions between suspicious stablecoins, foreign exchange, and gold trading.

The authorities also remain active in the fight against the black economy, including the proceeds of scams and other financial operations that may be suspicious. In total, scams cost the nation about 115 billion baht — or about $3.4 billion — in 2025 after sending about 173 million scam calls and text messages nationwide.

Regulatory direction reflects broader crypto policy

Thailand has maintained a split approach toward digital assets. The country’s regulatory framework allows the trading of cryptocurrencies. However, the central bank continues prohibiting stablecoin and digital asset payments for goods and services.

Meanwhile, trading activity remains active. CoinGecko data shows Bitkub processes around $26 million in daily trading volume. Nearly 40% of that activity comes from foreign exchange markets, while the USDT/THB pair remains the platform’s most traded market.

The latest review also follows additional enforcement actions earlier this year. Thai police recently uncovered a crypto laundering operation that allegedly processed proceeds from romance scams through multiple cryptocurrencies and cross-chain token swaps. Investigators said one suspect’s wallet handled more than $122.5 million within ten months.

Separately, Thailand’s SEC has continued refining digital asset regulation. Earlier proposals would allow licensed crypto businesses to offer digital asset derivatives without establishing separate corporate entities, following Cabinet-approved amendments recognizing digital assets as eligible underlying instruments for futures contracts.

The impact of enforcement goes beyond the market.

The new review has implications for exchanges, institutions and compliance teams in Thailand. Higher scrutiny could change transaction screening, customer due diligence and internal risk assessments in the way that companies operate.

The campaign also comes in the wake of doubts surrounding Thailand’s previous anti-scam campaign. In that same action, banks reportedly blocked some three million accounts and identified mule accounts and unusual financial transactions. But reports in the media also showed that thousands of legitimate businesses and people were also entangled in the enforcement.

Thailand’s stablecoin monitoring implies more regulatory control, not just more limitations on lawful crypto trading, for investors, exchanges, and financial institutions. Compliance requirements will be increasingly tough as detection becomes more sophisticated.

Conclusion

The monitoring of stablecoins in Thailand is part of a larger initiative to enhance financial supervision and reduce money laundering risks in the financial sector, including the digital assets sector. Now, authorities want to find suspicious activity sooner with coordinated supervision and better reporting requirements.

While cryptocurrency trading is still allowed, the Thailand stablecoin oversight should push for more compliance for companies dealing with USDT and other cryptocurrencies. Whether Thailand’s regulators can catch the wrongdoers while avoiding legions of disruption in the market is key to the effectiveness of the country’s stablecoin monitoring.