Key Insights:

- USDC transfers are settled in minutes, and all day long bank wires are settled in days and within specific hours.

- The USDC charges are minimal and transparent compared to the bank transfers that attract fees and FX spreads that increase the overall fee.

- USDC requires wallet-based knowledge and care, as bank transfer is less complicated and more popular.

Digital assets are a new form of money transfer being introduced worldwide and transforming the paradigm of money transfer. Cross-border payments are also made via USDC stablecoins and are cheaper and quicker than the conventional bank transfer method.

Both processes remain popular. However, they differ in terms of velocity, fees, availability, and how they operate. This guide explains how each system works and how it is most effective.

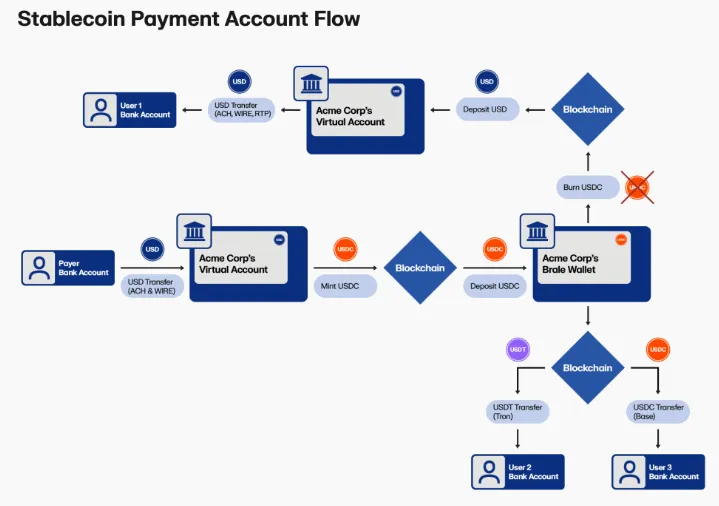

USDC Transfers operate through Blockchain Networks.

USDC is a pegged stablecoin of the U.S dollar. It works on blockchain networks, which are decentralized digital ledgers that record transactions without the involvement of banks.

Source: BVNK

Users can access it via crypto wallets (Coinbase Wallet, Trust Wallet, etc.). Digital assets can be safely stored, sent, and received using these wallets.

The initial step will be the conversion of fiat cash to USDC in a crypto exchange. Exchanges such as Binance are deposited using bank cheques, cards, or cell phones.

Once the conversion is made, the sender will be requested to type in the wallet address of the recipient and confirm the payment. Blockchain network transfers are executed in seconds or minutes, depending on the conditions of the networks.

Transactions are available 24/7 and are not limited by banking hours, weekends, or holidays.

Key Steps in a USDC Transfer

- Set up a crypto wallet.

- Exchange local currency for USDC.

- Type in the recipient wallet address.

- Confirm and submit the transaction.

- The money is paid to the recipient almost instantly.

For instance, an American sender can acquire the USDC in an exchange and send it directly to another person in Kenya.

The recipient can then exchange USDC for Kenyan shillings on peer-to-peer platforms and receive the funds via M-Pesa.

The entire process, that is, sending and receiving local currency on most occasions, can be accomplished in minutes.

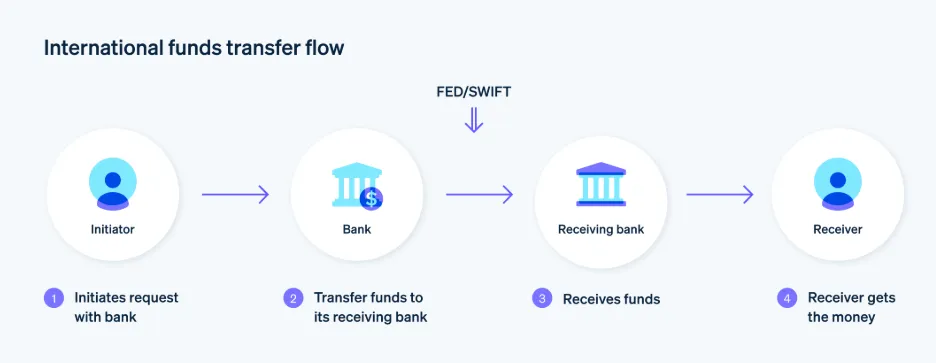

Bank transfers Track Multi-step financial networks

Conventional bank transfers are based on centralized financial institutions. Such transactions are frequently passed through several intermediary banks before reaching the actual beneficiary.

Source: Stripe

The sender triggers the transfer by entering the recipient’s account number and SWIFT code in the recipient bank details. The bank transacts the transaction after verifying the fees and exchange rates.

The funds take 1-5 business days to arrive. Delays could be due to compliance checks, time zones, or non-working days.

Example: Bank Transfer to Kenya

A sender in the United Kingdom transfers funds to a Kenyan account held at KCB Bank or Equity Bank.

The transaction passes through intermediary banks before reaching the destination. Afterward, the recipient may transfer funds to M-Pesa, adding additional time and cost.

Differences in speed and cost characterize the Choice

The biggest difference between USDC and bank transfers is the speed of transacting.

USDC transfers are nearly instant and are continuous. In contrast, bank transfers require banking hours and may take several days to be realised.

There is also a significant cost difference. Transactions using USDC do not incur significant network charges, as the network determines these the user uses. There are also service charges and foreign exchange margins added to bank transfers, which makes them even more expensive.

The two systems are also further divided by availability. USDC is time-free, whereas banks adhere to regular schedules and close operations during weekends and holidays.

Accessibility and Risk Factors

Bank transfers are more accessible to the majority of users. A large number of people already have bank accounts and know how to manage them.

USDC must have a fundamental understanding of crypto wallets and blockchain transactions. Users are expected to take good care of wallet addresses since once a transaction is confirmed, it cannot be undone.

“Digital asset transfers can reduce settlement time significantly, but they require user responsibility in handling private keys and addresses,” said a fintech analyst familiar with cross-border payment systems.

Both systems offer strong security when used correctly. Nevertheless, any misplaced crypto transaction may result in irreparable financial loss.

Use Cases Keep on splitting up

The USDC is increasingly becoming the currency used in making frequent cross-border payments and remittances. It is speedy and cheaper, hence applicable in emergency transfers.

Big transactions, controlled payments, and users who do not have access to cryptocurrency platforms can still use bank transfers to carry out such transactions.

The use of blockchain-based systems in peer-to-peer and international payment transactions is growing, though the compliance-based transactions remain dominated by financial institutions.

Final Overview

USDC offers a cheaper, quicker method of international transfers by eliminating intermediaries and long lines.

Bank transfers are also more popular and controlled, but they are more expensive and take longer to process.

The two systems are used for different requirements. The decision will be based on the user’s familiarity, urgency, and availability of digital financial instruments.