Key Insights:

- The Fed opened a 60-day comment period on its reputational risk proposal.

- The regulation would eliminate reputational risk in the bank supervision policy.

- The move was associated with the issue of debanking by lawmakers and crypto leaders.

The Federal Reserve reputational risk proposal has entered a formal 60-day public comment period, marking a significant regulatory step toward permanently removing “reputational risk” from the central bank’s supervisory framework.

The move follows prior announcements and supervisory guidance issued last year and is viewed by crypto industry participants as a decisive development in the broader debate surrounding debanking and what has been referred to as Operation Choke Point 2.0.

Federal Reserve Reputational Risk Policy Shift Moves Toward Permanence

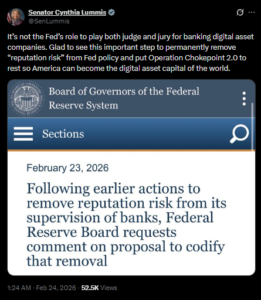

In a press release issued Monday, the Federal Reserve confirmed that it is seeking public input on the proposal before finalizing the rule. Once the 60-day comment window closes, a final version is expected to be published in the Federal Register.

The Federal Reserve’s reputational risk framework began to change in June last year, when the central bank stated that it had directed supervisors to stop encouraging or pressuring banks to close customer accounts based on reputational concerns.

Source: Senator Cynthia Lummis

Under the revised approach, supervisory decisions are limited to assessments of material financial risks rather than subjective concerns about how a client’s activities might affect a bank’s public image.

The current proposal would permanently eliminate reputational risk as a factor in supervision and formally embed the updated standard into regulatory policy. According to the Federal Reserve, supervisory evaluations would continue to center on financial risk management, including safety and soundness considerations.

In a statement issued on Tuesday, Vice Chair for Supervision Michelle Bowman noted that due to the abstract definition and subjectivity of the standard, there was inconsistency in oversight practices, and also that it drew attention to the clearly identifiable financial risks, such as credit, liquidity, and market exposures that directly affect the stability and resilience of the banking institutions.

Her remarks referenced broader allegations that reputational risk concerns were used to justify account closures involving politically exposed individuals or businesses operating in lawful but controversial sectors.

Operation Choke Point 2.0 Allegations and Political Response

Crypto industry figures have used the term Operation Choke Point 2.0 to describe what they characterize as coordinated regulatory pressure aimed at limiting banking access for digital asset companies during the previous administration. The phrase draws comparisons to an earlier Department of Justice initiative unrelated to crypto.

The Federal Reserve’s reputational risk proposal follows actions taken by the current administration to address concerns about debanking. Last August, President Donald Trump signed an executive order directing federal banking regulators to adopt policies preventing what the White House described as “politicized or unlawful debanking.” At the time, the administration stated it had “ended Operation Chokepoint 2.0 once and for all.”

Trump had also previously worked on a draft order calling on bank regulators to investigate allegations of debanking raised by industry participants.

An example frequently cited in the debate involves JPMorgan Chase’s closure of accounts belonging to members of the Trump family.

According to a recent Associated Press report, JPMorgan acknowledged that it closed President Donald Trump’s accounts after the January 6, 2021, attack on the U.S. Capitol.

Trump has since filed a lawsuit against JPMorgan seeking $5 billion in damages, alleging politically motivated account closures. Fox Business reporter Charles Gasparino reported that multiple banks acted under pressure tied to Office of the Comptroller of the Currency supervisory standards involving reputational risk.

Industry and Lawmaker Reactions

Several lawmakers and industry representatives publicly responded to the Federal Reserve’s proposal on reputational risk.

Senator Cynthia Lummis commented on the social media platform X that it is “not the Fed’s role to play both judge and jury for banking digital asset companies.”

She added that permanently removing reputational risk from Federal Reserve policy would help put Operation Choke Point 2.0 to rest.

Alex Thorn, head of firmwide research at Galaxy Digital, also commented on X, stating that the “chokepoint 2.0 rollback continues.”

Head of firmwide research at Galaxy Digital, Source: Alex Thorn

The comment period announcement comes amid additional regulatory developments related to past supervisory actions involving crypto firms. Earlier this month, the Federal Deposit Insurance Corporation settled a Freedom of Information Act lawsuit brought at the direction of Coinbase.

Under the settlement, the FDIC agreed to pay $188,440 in legal fees after a court found the agency had violated FOIA by categorically withholding dozens of crypto-related “pause letters.” Those documents indicated that banks were pressed to halt or limit crypto activity during the Biden administration.

As part of the agreement, the FDIC committed to revising its FOIA training materials and stated that it would no longer maintain a blanket policy of categorically withholding bank supervisory documents.